Dickssporting Goods Credit Card Login – Secure Access

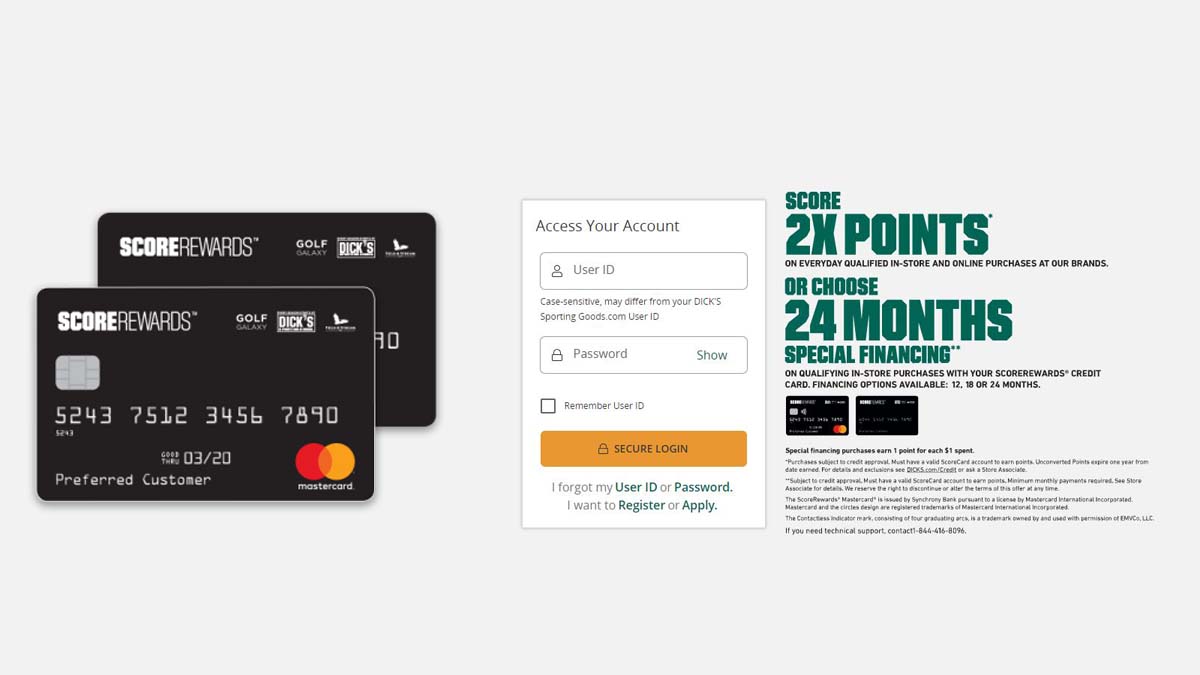

Do you have a Dick’s Sporting Goods ScoreRewards® Credit Card and need to manage your account online? You can’t access your statement or rewards details directly through the DICK’s Sporting Goods website. That’s because your credit card is actually serviced by Synchrony, a financial services company. In the next section, we’ll provide you with the […]