How to Set and Achieve Personal Finance Goals

Ready to take charge of your wallet? Discover the secrets to setting and crushing your personal finance goals. Your bank account will thank you later!

Ready to take charge of your wallet? Discover the secrets to setting and crushing your personal finance goals. Your bank account will thank you later!

Discover how financial advisors can turbocharge your Finance and Investing journey. Get expert guidance, avoid costly mistakes, and build wealth like a pro!

Dodge these 5 personal finance blunders and keep your wallet happy! Learn how to outsmart common money mistakes and build a brighter financial future.

Ready to turbocharge your retirement nest egg? Dive into smart finance and investing strategies that’ll make your golden years shine brighter than a freshly minted coin.

Ready to adult like a pro? Dive into smart personal finance strategies for young professionals. Learn to budget, invest, and save without sacrificing your avocado toast habit.

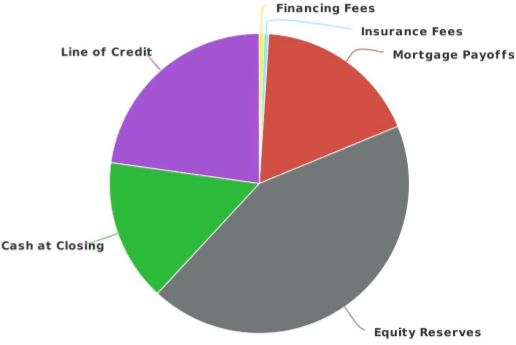

A reverse mortgage calculator is a valuable financial tool for homeowners aged 62 or older who are considering using their home equity to supplement their retirement income. Unlike traditional mortgages, where you borrow money to purchase a home and repay the loan over time, a reverse mortgage allows you to access the equity in your […]

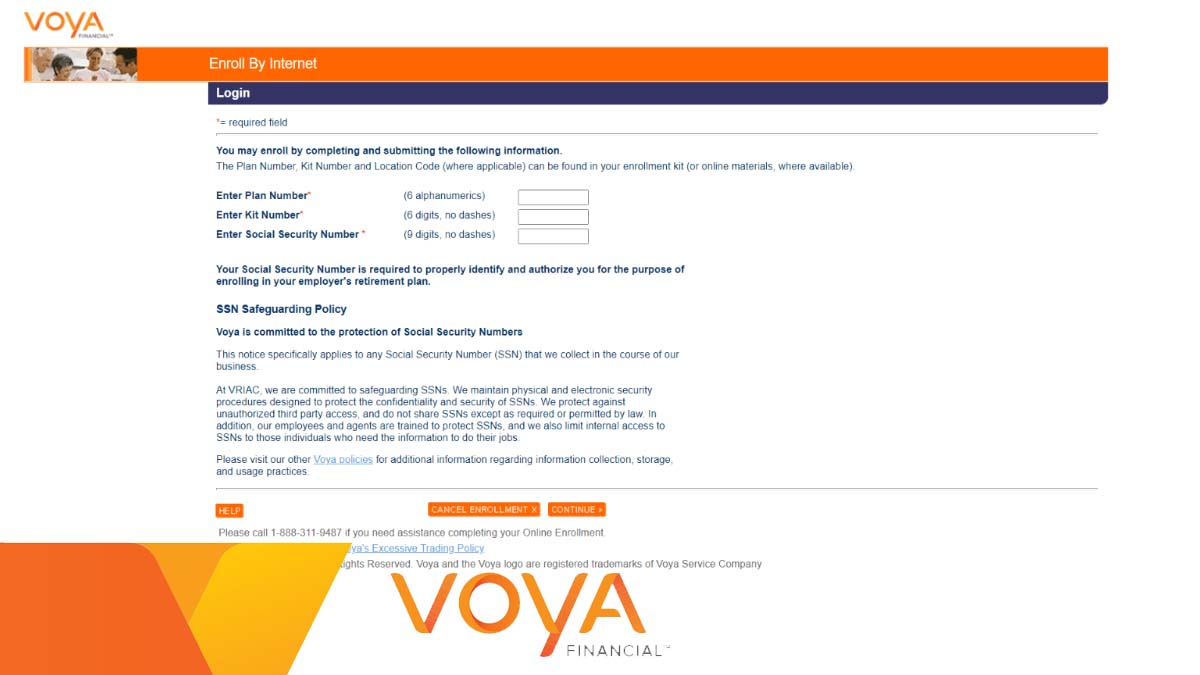

Secure your future today. Take control of your retirement savings with Voya Financial. Visit www.voyaretirementplans.com and register now to access your employer-sponsored retirement plan and start building a brighter tomorrow. Retirement may seem like a distant horizon, especially for young professionals just starting their careers. However, securing your financial future requires taking proactive steps early […]