In the dynamic mortgage lending landscape, RoundPoint Mortgage has emerged as a reliable and innovative player. For homeowners considering refinancing their existing mortgage, RoundPoint offers a variety of options designed to meet individual needs and financial goals. This article will delve into the potential benefits of refinancing with RoundPoint Mortgage, the company’s commitment to customer satisfaction, and the steps involved in the process.

Whether seeking to lower monthly payments, shorten loan terms, or access home equity, refinancing with RoundPoint Mortgage could be a strategic move. By harnessing RoundPoint’s expertise and leveraging competitive interest rates, homeowners can improve their financial outlook and unlock the full potential of their homeownership journey.

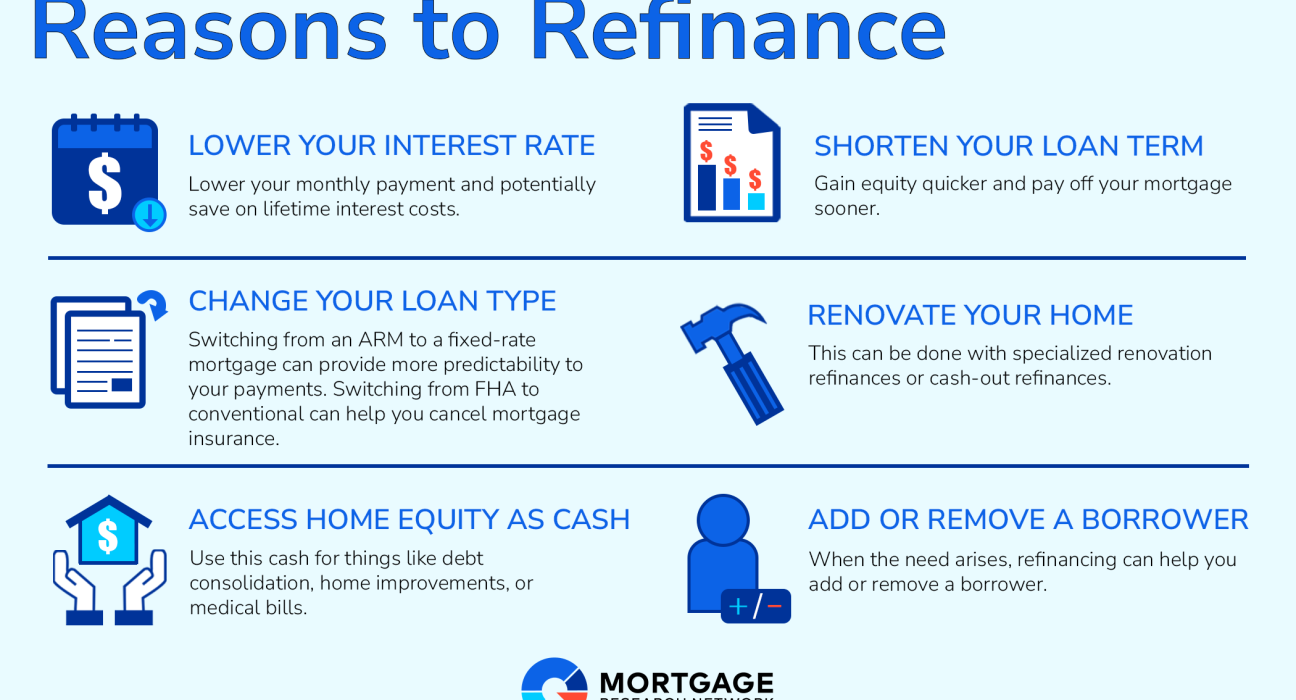

Benefits of Refinancing with RoundPoint Mortgage

Refinancing with RoundPoint Mortgage could offer several potential benefits, depending on your individual financial situation and goals. Here are some possible advantages:

- Lower Interest Rate: If market interest rates have dropped since you obtained your original mortgage, refinancing with RoundPoint could potentially secure a lower interest rate, leading to decreased monthly payments and overall interest savings throughout the life of the loan.

- Shorter Loan Term: Refinancing into a shorter-term loan could allow you to pay off your mortgage sooner, saving you money on interest over the long run. However, this typically results in higher monthly payments.

- Cash-Out Refinance: This option enables you to access a portion of your home’s equity in cash, which can be utilized for various purposes such as home improvements, debt consolidation, or other financial needs.

- Switch from an Adjustable-Rate to a Fixed-Rate Mortgage: Refinancing from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage provides stability and predictability by locking in a constant interest rate for the entire loan term, protecting you from potential interest rate increases in the future.

- Debt Consolidation: If you have high-interest debts, such as credit cards or personal loans, refinancing your mortgage and taking cash out could allow you to consolidate those debts into a single lower-interest loan, potentially simplifying your finances and saving money on interest.

However, it’s important to remember that refinancing also involves closing costs and fees, which need to be factored into your decision. It’s advisable to carefully consider your financial goals and circumstances, compare offers from different lenders, and consult with a financial advisor to ensure that refinancing is the right choice for you.

Eligibility Requirements and Documentation

1. Eligibility Check

- Credit Score: Highlight the minimum credit score needed and explain how a higher score might lead to better rates.

- Debt-to-Income Ratio (DTI): Explain DTI and its importance in the approval process.

- Home Equity: Clarify how much equity is typically required for refinancing.

- Loan Type: Specify if RoundPoint has any restrictions on the types of loans they refinance (e.g., conventional, FHA, VA).

2. Documentation Gathering

- Income Verification: List the documents typically required to prove income (e.g., pay stubs, tax returns, W-2s).

- Asset Verification: Explain the need to show available funds for closing costs and reserves.

- Property Documentation: Mention documents like the current mortgage statement, homeowners insurance policy, and property tax bill.

3. Application & Underwriting

- Application Submission: Describe the online or in-person application process.

- Underwriting Review: Explain how RoundPoint evaluates the application and supporting documents.

- Appraisal: Mention the potential need for a home appraisal.

4. Closing

- Closing Disclosure: Explain the importance of reviewing this document carefully before closing.

- The Closing Costs: Discuss the various fees associated with closing and how they can be paid.

- Final Loan Documents: Highlight the signing of the new loan agreement and other legal documents.

Step-by-Step Guide on How to Refinance

Refinancing your mortgage with RoundPoint can be a smooth process if you break it down into manageable steps. Here’s how to tackle it:

- Check Your Eligibility: Start by understanding RoundPoint’s requirements. What credit score do they prefer? What’s their ideal debt-to-income ratio? Do you have enough equity in your home?

- Gather Your Documents: Collect all your financial information. You’ll likely need pay stubs, tax returns, bank statements, and your current mortgage details.

- Complete the Application: RoundPoint offers an online application, so have all your info handy and fill it out carefully.

- Await Underwriting: This is where RoundPoint reviews your application and makes a decision. Be patient and responsive to any requests for additional information.

- Close on Your New Loan: Once approved, you’ll sign the final paperwork and your new mortgage will be in place.

Tips for Getting the Best Refinance Deal

Here are some tips to secure the best rates and terms with RoundPoint:

- Boost Your Credit Score: A higher credit score often translates to lower interest rates.Pay down credit card debt, avoid opening new accounts, and dispute any errors on your credit report.

- Lower Your Debt-to-Income Ratio: Lenders love borrowers with low debt. If you can pay off some loans or increase your income before applying, it can significantly improve your chances of getting a great deal.

- Build Your Home Equity: The more equity you have in your home, the more attractive you’ll be to lenders. Consider making extra mortgage payments or waiting until you’ve built up more equity before refinancing.

- Shop Around and Compare Offers: Don’t settle for the first offer! Compare interest rates, closing costs, and terms from multiple lenders to ensure you’re getting the best deal.

- Consider a Shorter Loan Term: While it may increase your monthly payment, a shorter loan term can save you thousands in interest over the life of the loan.

- Ask About Discount Points: Paying points upfront can reduce your interest rate. Calculate whether the long-term savings outweigh the upfront cost.

- Be Prepared for Closing Costs: Refinancing comes with closing costs, so factor them into your decision. Ask about any lender fees or discounts that might be available.

- Communicate with Your Loan Officer: Keep the lines of communication open and be responsive to any requests for information. This will help the process run smoothly and increase your chances of a successful refinance.

Remember, knowledge is power! By understanding the process and preparing yourself financially, you’ll be well-equipped to negotiate the best refinance deal with RoundPoint.