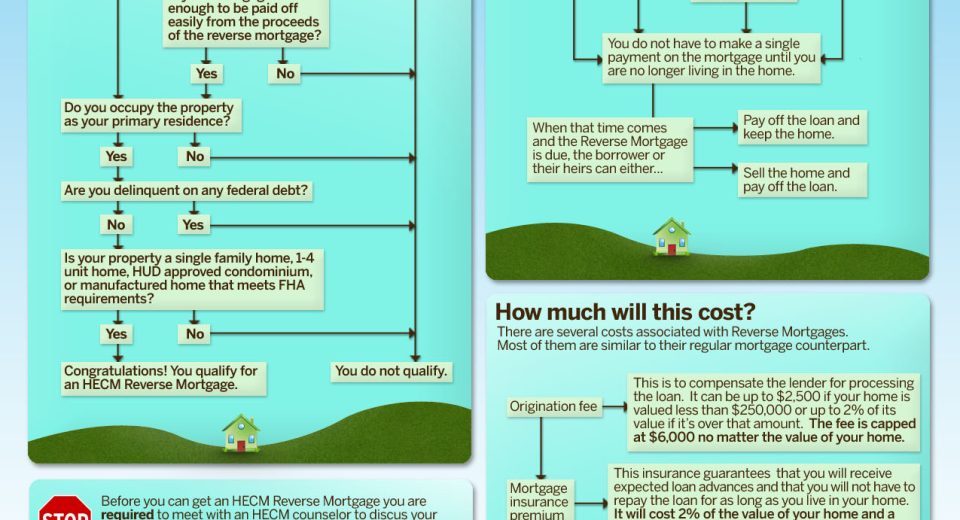

Reverse Mortgage Application Process – A Step-by-Step Guide

Navigating the path to a reverse mortgage involves understanding its application process, a journey with distinct stages and requirements. This process empowers homeowners aged 62 and above to tap into their home equity without selling their property, providing financial flexibility during retirement. Learn the reverse mortgage application process. Learn about eligibility, required documents, and steps […]