Navigating the path to a reverse mortgage involves understanding its application process, a journey with distinct stages and requirements. This process empowers homeowners aged 62 and above to tap into their home equity without selling their property, providing financial flexibility during retirement. Learn the reverse mortgage application process. Learn about eligibility, required documents, and steps involved from start to finish.

From initial eligibility assessment and mandatory counseling to detailed financial and property evaluations, each step in the application ensures both the lender’s and borrower’s interests are protected. The process concludes with a loan closing, where homeowners gain access to their chosen disbursement method, whether a lump sum, line of credit, or monthly payments.

Understanding Reverse Mortgages

- What is a Reverse Mortgage? It’s a type of loan that allows you to convert a portion of your home equity into cash. Unlike traditional mortgages, you don’t have to make monthly payments. The loan is typically repaid when you sell the home, move out permanently, or pass away.

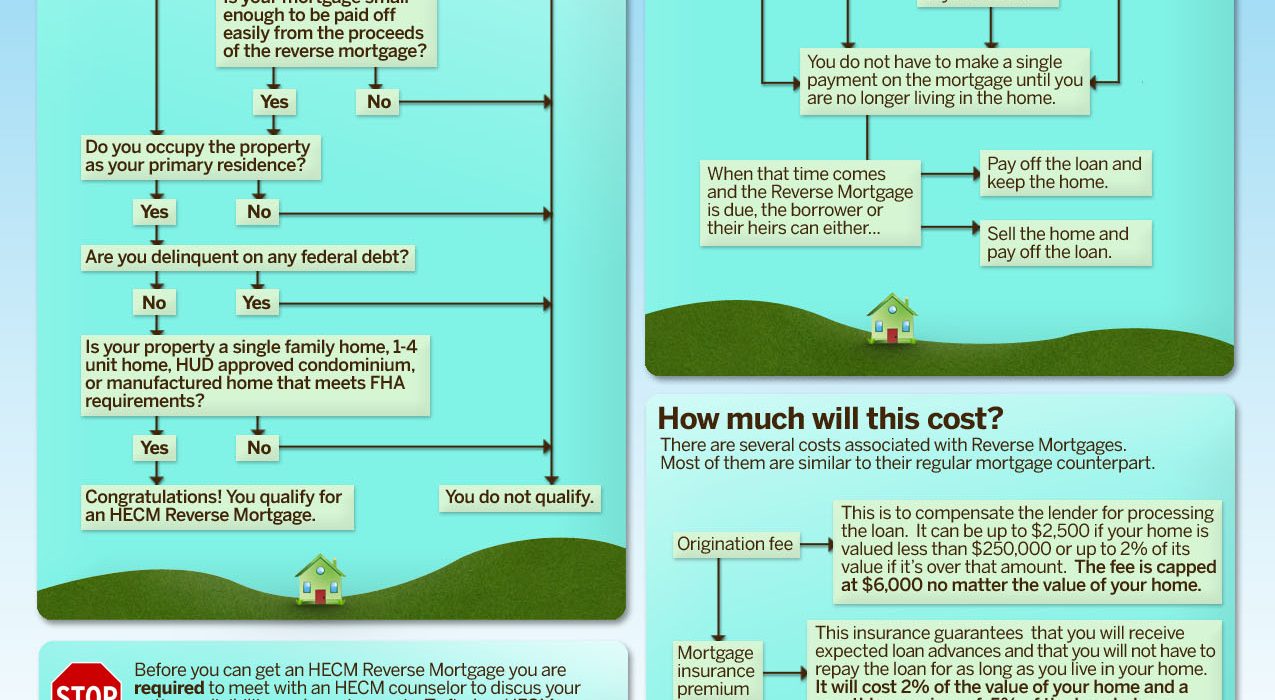

- Eligibility Requirements: To qualify, you generally must be at least 62 years old, own your home outright or have a low mortgage balance, and live in the home as your primary residence.

- Types of Reverse Mortgages: The most common type is the Home Equity Conversion Mortgage (HECM), insured by the Federal Housing Administration (FHA). There are also proprietary reverse mortgages offered by private lenders.

The Reverse Mortgage Application Process

The reverse mortgage application process involves several crucial steps:

1. Counseling:

- Mandatory Requirement: Before applying, you must complete counseling with a HUD-approved counselor.

- Purpose: The counseling session aims to ensure you fully understand the terms, benefits, and potential drawbacks of a reverse mortgage.

- Topics Covered: The counselor will discuss eligibility requirements, loan options, financial implications, and alternatives to reverse mortgages.

2. Choosing a Lender:

- Research: Compare offers from different lenders, considering interest rates, fees, and customer service.

- Reputation: Choose a lender with a solid reputation and experience in reverse mortgages.

- Questions: Ask potential lenders about their specific requirements and the application process.

3. Application Submission:

- Documentation: Gather necessary documents, including proof of age, income, homeownership, and current mortgage information.

- Completeness: Ensure your application is complete and accurate to avoid delays.

- Assistance: Your lender or a housing counselor can help you complete the application if needed.

4. Home Appraisal:

- Purpose: An appraisal determines your home’s current market value, which affects the loan amount you can receive.

- Appraiser Selection: The lender will typically select an appraiser, but you may have some input.

- Accessibility: Ensure the appraiser has access to all areas of your home for a thorough evaluation.

5. Underwriting and Approval:

- Review: The lender’s underwriters will review your application, appraisal, and financial information.

- Credit Check: Your credit history will be evaluated, but a perfect score isn’t required.

- Decision: You’ll receive a loan approval or denial based on the underwriting review.

6. Closing:

- Review Documents: Carefully review all loan documents before signing.

- Legal Representation: Consider consulting an attorney to ensure you understand the terms and implications.

- Funds Disbursement: After closing, you’ll receive the funds according to the chosen disbursement option (lump sum, line of credit, or monthly payments).

Factors Affecting Eligibility

Several factors influence your eligibility for a reverse mortgage:

- Age: You must be at least 62 years old.

- Homeownership: You must own your home outright or have a low remaining mortgage balance.

- Primary Residence: The home must be your primary residence.

- Financial Assessment: You must demonstrate the ability to pay property taxes, and insurance, and maintain the home.

FAQs

Who is eligible for a reverse mortgage?

To be eligible, you must be at least 62 years old, own your home outright or have a low mortgage balance, and occupy the home as your primary residence.

What are the costs associated with a reverse mortgage?

Costs can include origination fees, closing costs, mortgage insurance premiums, and servicing fees. It’s essential to understand these costs upfront.

Can I still sell my home if I have a reverse mortgage?

Yes, you retain ownership of your home and can sell it at any time. The proceeds from the sale will be used to repay the reverse mortgage loan.

What happens if I pass away or move out of my home?

The loan becomes due and payable when you pass away, sell the home, or no longer live in it as your primary residence.

How can I use the funds from a reverse mortgage?

You can use the funds for various purposes, including supplementing retirement income, covering healthcare expenses, home repairs, or even travel.

Conclusion

The reverse mortgage application process can be navigated successfully with careful planning and understanding. By following the outlined steps, researching lenders, and seeking professional guidance, you can make an informed decision about whether a reverse mortgage is the right financial solution for you.

Remember: This article provides general information about the reverse mortgage application process. It’s crucial to consult with a HUD-approved counselor and financial advisor to assess your individual circumstances and determine the best course of action.